RISR Commentary for September 2022

Performance Summary

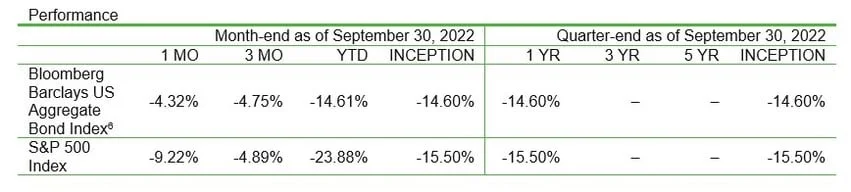

The FolioBeyond Rising Rates ETF (ticker: RISR) returned 3.90 % based on the closing market price (4.21% based on net asset value or “NAV”) in September. In comparison, the ICET7IN Index (US Treasury 7 Year Bond Inversed Index) returned 5.07% while the Bloomberg Barclays U.S. Aggregate Bond Index ("AGG") returned -4.14% during the same period. This performance lagged slightly, but was reasonably close to the fund’s target duration, as the 10-year treasury yield moved up by roughly 59 basis points (bps) during the month. The slippage was attributable to some OAS widening for MBS IOs connected with overall market volatility, plus some surrender of bid-ask spreads we encountered due to share redemptions.

During September, investor confidence continued to erode, and talk of an economic hard-landing combined with persistent inflation crowded out earlier discussions of peak inflation and soft-landings. “Stagflation” is an ugly word, a portmanteau of inflation and stagnation. It was coined in the1970s to describe an economic environment that was generally not thought to be possible. Standard economic theory taught that inflation was associated with a rapidly growing, “over-heated” economy. Stagnation or recession on the other hand, was thought to be associated with disinflation. On the other hand, stagnation or recession was thought to be associated with disinflation. This relationship even had its own graph, the “Phillips” curve. It looked basically like this:

Economic theory, and economic policy makers, did not consider the possibility of high inflation and high unemployment occurring at the same time. And then they were mugged by reality, and a new word— stagflation—had to be invented to describe it.

It has been a long time since the 1970s, far longer than the careers of many asset managers, and market commentators working today. But is seems we may be headed that way again. Markets in September saw a persistence in high, or even accelerating inflation with undeniable signs of an emerging economic slowdown. Hundreds of companies from autos to retailing to tech have announced significant layoffs, even as the reported unemployment rate remained low. A large part of that is related to the reluctance of millions of workers who became unemployed during Covid to return to the workforce. But an important early indicator—the ratio of unemployed workers to job openings—has flattened after reaching an historic low over the summer. The recession that the Fed’s interest rate policies are precipitating may be the first one in which employment and economic activity generally decline, but in which the headline unemployment rate does not reach peak levels, due to suppressed labor participation rates. We may need to coin another word for what is coming our way.

Last month, we discussed the movements in the spread between short-term and long-term interest rates. The yield curve remains inverted—short term rates are higher than long-term rates—but that appears to be coming to an end. Historically, inverted yield curves have been strong indicators of an impending economic slowdown, but such inversions tend to be relatively short-lived. That seems to be the pattern this time, as well. The graph below shows the trend in 2s/10s since the beginning of 2022. The flattening and inverting yield-curve trend has been significant, but since the summer, would seem to be bottoming out. If this occurs, it will be positive for RISR, since a steeper yield curve further reduces mortgage prepayment speeds, which ought to have a positive impact on MBS IO values.

Outlook

As we noted last month, markets were shocked out of their complacency by a very concise and unambiguous Jackson Hole speech by Fed Chair Jay Powell, in which he removed any doubt that they intended to break the back of inflation, despite the near certainty it would lead to economic hardship. This reality caused the 10-year Treasury to surge to nearly 4%, although a few basis points were given back in a brief flight to quality that followed some terrible policy statements coming from the UK.

The question now becomes, how much hardship is the economy in for? There is a growing consensus that the recession ahead of us (some argue it has already begun) may be more severe than markets expected just a few months ago. Over the summer there was lots of talk about a “soft landing” in which the Fed gently guides the economy down like a pilot bringing a 737 into JFK. Frankly, that was never a high probability scenario, in our view. The market consensus seems to have come around to our point of view on this.

Rather than a soft landing, we believe it is going to take a sustained campaign by the Fed to raise interest rates much higher and keep them there longer than many folks think, to wring the inflationary pressures out of the economy. Their job is being made more difficult by several factors:

Fiscal policy makers seem determined to continue to launch massive spending programs including the comically named Inflation Reduction Act, student loan forgiveness and many other programs, that are transparent attempts to buy votes in the upcoming midterm elections.

Energy prices will surely resume their rise following a period of softening over the summer, due to winter heating needs, the lack of supply from Russia, and newly announced production cutbacks by OPEC. While perhaps understandable from a public policy perspective, attempts by policy makers to soften the blow from these energy price hikes through bureaucratically imposed price ”caps” (really a form of subsidy to energy consumption), will have the effect of exacerbating and reinforcing these supply shocks by stimulating demand.

China’s zero-covid policy is wreaking havoc on global supply chain problems as whole cities go into sudden lockdowns, and then reopen.

The ongoing war in Ukraine shows no signs of coming to resolution, and this is having a wide range of knock-on effects on food supplies, among other stresses.

Despite sharp increases in mortgage rates, housing prices remain elevated because of a decades long imbalance between home building and rates of household formation. We have many fewer dwelling units in the US than we need.

All of these factors and more support continued inflationary pressures, that will be difficult to resolve. In addition, as Nobel prize-winning monetary economist Milton Friedman said, “Monetary policy acts with long and variable lags.” People tend to forget the “long” part of that aphorism. The Fed only launched its restrictive policy stance in March of this year. Even after five rate hikes, we are still looking at a 10-year Treasury rate that is significantly below historical norms and far below the rate of inflation.

And yet many market participants and economic commentators have been calling on the Fed to slow the pace of its rate hikes. We do not think they will, nor should they. Raising interest rates brings inflation down by altering the incentive structures and time preferences for individuals and businesses. This is usually referred to as reducing aggregate demand, but it is more complicated than that. Expectations matter greatly. To over-simplify a bit, if people think there will be inflation, then there will be inflation. When interest rates are high enough for long enough to alter that outlook, it affects their consumption and production choices, and inflation recedes. That takes time, historically years, not months or quarters.

Even if the Fed does go wobbly in the short run, though, RISR investors will be well served (RISR’s 30 Day SEC Yield as of September 30, 2022, is 6.77%). In addition, RISR has a low or negative correlation to equities and the overall bond market.

By adding an allocation to RISR, many investors could achieve a meaningful reduction in overall portfolio volatility without sacrificing current income. The table below shows the impact of adding various allocations of RISR to different portfolio mixes and benchmarks:

It is impossible to know ahead of time what it will take to bring inflationary pressures under control. A growing number of prominent voices have been saying what we have been saying for some time. Indeed, some older hands including Mark Mobius have recently suggested that a Fed Funds rate of 6% or even higher may be needed. At their September meeting, virtually all the Fed governors raised their expectation of the so-called terminal rate for Fed Funds, with the consensus now approaching 5%, up from something like 3% just a few months ago. We reached 3.25% in September, and there is no sign of stopping. Events are moving quickly.

For investors who share our view, or even those who only want to prepare for the possibility, we think RISR can still contribute importantly to your overall strategy. No matter if the Fed goes to 4% and pauses or is forced to go much higher as we believe adding RISR can sharply reduce the interest rate risk in your current portfolio by reducing duration and volatility, and adding a meaningful degree of current income potential from dividends. RISR’s most recent cash dividend of 6.7% (September 30, 2022 30 Day SEC Yield), is materially higher than that of the IBOXHY Index which pays 5.83%. And since RISRs investments are issued by government sponsored entities, we don’t subject investors to nearly the same credit risk as does the IBOXHY Index. If rates continue to rise, we will invest fresh capital in progressively higher mortgage coupon rates, which should increase our dividend accordingly.

As we have noted previously, our strategy aims to generally hold a negative 10-year duration. That is, the fund is managed to experience price movements of 10x the change in interest rates. Consequently, if rates were to rise 100bps, we would expect to see gains in NAV per share of around 10%. A 200 bps rise could see a 20% gain, and so on. We continue to believe this trade has a long way to run. Even if it takes the Fed takes a break from hiking rates later in 2022, volatility seems to show no sign of abating. We believe under these circumstances, the benefits of holding RISR can be substantial for a broad class of investors. We would be pleased to discuss your particular situation to explore how best to incorporate RISR into your overall portfolio.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 866-497-4963. Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Returns beyond 1 year are annualized.

A fund's NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the fund was traded. The fund intends to pay out income, if any, monthly. There is no guarantee these distributions will be made.

Total Expense Ratio is 1.01%.

For standardized performance click here.

Portfolio Applications

We believe RISR provides an attractive, thematic strategy that provide strong correlation benefits for both fixed income and equity portfolios. It can be utilized as part of a core holding for diversified portfolios or as an overlay to manage the interest rate risk of fixed income portfolios. Alternatively, RISR can be used as a macro hedge against rising interest rates with less exposure to equity beta and negative correlation to fixed income beta. The underlying bonds are all U.S. agency credit that are guaranteed by FNMA, FHLMC or GNMA. There is no financing leverage or explicit short positions that relies on borrowed securities. Also, timing is on our side as the strategy generates current income if interest rates were to remain within a trading range.

Please contact us to explore how RISR can be utilized as a unique tool to adjust your portfolio allocations in the current inflationary environment.

| Yung Lim | Dean Smith | George Lucaci |

|---|---|---|

| Chief Executive Officer | Chief Strategist and Marketing Officer | Global Head of Distribution |

| Chief Investment Officer | RISR Portfolio Manager | |

| ylim@foliobeyond.com | dsmith@foliobeyond.com | glucaci@foliobeyond.com |

| 917-892-9075 | 914-523-2180 | 908-723-3372 |

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus with this and other information about the Fund, please call (866) 497-4963 or visit our website at www.etfs.foliobeyond.com. Read the prospectus or summary prospectus carefully before investing.

Investments involve risk. Principal loss is possible. Unlike mutual funds, ETFs may trade at a premium or discount to their net asset value. The fund is new and has limited operating history to judge fund risks. The value of MBS IOs is more volatile than other types of mortgage related securities. They are very sensitive not only to declining interest rates, but also to the rate of prepayments. MBS IOs involve the risk that borrowers may default on their mortgage obligations or the guarantees underlying the mortgage-backed securities will default or otherwise fail and that, during periods of falling interest rates, mortgage-backed securities will be called or prepaid, which may result in the Fund having to reinvest proceeds in other investments at a lower interest rate.

The Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying assets or index; the loss of principal, including the potential loss of amounts greater than the initial amount invested in the derivative instrument. The value of the Fund’s investments in fixed income securities (not including MBS IOs) will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities owned indirectly by the Fund. Please see the prospectus for a complete description of principal risks.

Diversification does not eliminate the risk of experiencing investment losses.

Index Definitions

Bloomberg Barclays US Aggregate Bond Index: A broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

US Treasury 7-10 Yr Bond Inverse Index: ICE U.S. Treasury 7-10 Year Bond 1X Inverse Index is designed to provide the inverse of the daily return of the ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7). ICE U.S. Treasury 7-10 Year Bond Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market. Qualifying securities of the underlying index must have greater than or equal to seven years and less than 10 years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million.

S&P 500 (Standard & Poors 500): The S&P 500 Index represents a market-capitalization weighted index of 500 leading publicly traded companies in the U.S, as defined by the Standard & Poors corporation.

Definitions

Alpha: a return achieved above and beyond the return of a benchmark or proxy with a similar risk level.

Basis Points (bps): Is a unit of measure used in quoting yields, changes in yields or differences between yields. One basis point is equal to 0.01%, or one one-hundredth of a percent of yield and 100 basis points equals 1%.

Beta measures: the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index; more than one means greater volatility.

Coupon: is the annual interest rate paid on a bond, expressed as a percentage of the bond’s face value.

Convexity: A measure of how the duration of a bond changes in correlation to an interest rate change. The greater the convexity of a bond the greater the exposure of interest rate risk to the portfolio.

CUSIP: An identifier number that stands for the Committee on Uniform Securities Identification Procedures assigned to stocks and registered bonds in the United States and Canada.

Duration: measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

GNMA: Government National Mortgage Association

FNMA: Federal National Mortgage Association

FHLMC: Federal Home Loan Mortgage Corporation

Producer Price Index (PPI) : is a family of indexes that measures the average change over time in selling prices received by domestic producers of goods and services. PPIs measure price change from the perspective of the seller. This contrasts with other measures, such as the Consumer Price Index (CPI), that measure price change from the purchaser's perspective. Sellers' and purchasers' prices may differ due to government subsidies, sales and excise taxes, and distribution costs.

Short Investment (Shorting): is a position that has been sold with the expectation that it will decrease in value, the intention being to repurchase it later at a lower price.

Distributed by Foreside Fund Services, LLC.