RISR Commentary for December 2023

Click here for a pdf version of this commentary.

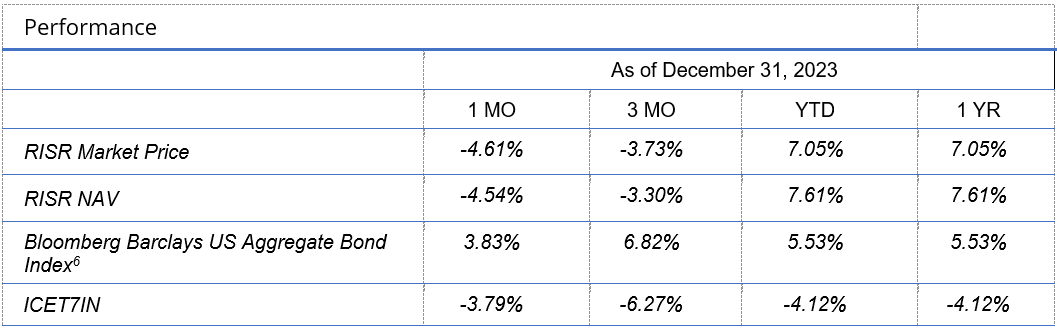

Performance Summary

The FolioBeyond Alternative Income and Interest Rate Hedge ETF (ticker: RISR) returned -4.61% based on the closing market price (-4.54% based on net asset value or “NAV”) in December. In comparison, the ICET7IN Index (US Treasury 7-Year Bond Inversed Index) returned -3.79% while the Bloomberg Barclays U.S. Aggregate Bond Index ("AGG") returned 3.83% during the same period.

This brought the full year return to 7.05% (7.61% based on NAV). This performance was obtained over the course of a roller-coaster year where the 10-year treasury yield ranged from a low of 3.31% to a high of 4.99%, but finished the year within 2 basis points of where it started.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 866-497-4963. Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Returns beyond 1 year are annualized.

A fund's NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the fund was traded. The fund intends to pay out income, if any, monthly. There is no guarantee these distributions will be made.

Total Expense Ratio is 0.99%.

For standardized performance click here

In short, 2023 was one of the most volatile rate markets in recent memory. The steady grind higher in rates that occurred from April until late October, was almost totally reversed in the last several weeks of the year. In fact, the sharp drop in rates that occurred in November and December was the largest observed since the 2008 financial crisis, and the second largest 2-month decline since 1998. So, what happened?

As we noted last month, some observers had perceived a slight softening in a couple of recent economic indicators related to the labor market, and took this as a sign that the Federal Reserve’s policy of higher rates would have to be halted or even reversed. This was further compounded by press conference in mid-December at which Chair Jay Powel almost imperceptibly softened his language relating Fed policy going forward. But this was all the bulls need to hear, and a massive bond rally followed.

In the days that followed, numerous other Fed speakers pushed back against the market sentiment, suggesting it was an over-reading of situation, but these messages were largely ignored. When a strong market thesis gets adopted, it is often the case that people hear what they want to hear. Bond investors very much want to hear that rates will be falling and prices will be rising going forward, and are ignoring evidence to the contrary. In our view this is a mistake, and a misreading of the economic indicators and the Fed’s actual messaging. We will return to this idea, below.

Regardless, the performance of RISR over the last few months, and indeed for the whole year, was almost exactly as we intended our strategy to work. The fund increased in value as rates rose, and declined as rates fell. We closed 2022 at 31.59 per share, and the last traded price of 2023 was 31.30 per share, which is highly consistent with the nearly unchanged level of market interest rates, noted above. Meanwhile our dividend distributions of $2.493/per share resulted in a total return of 7.05% for the full year. Investors who held RISR as part of a larger fixed income portfolio, would have seen lower overall volatility and attractive regular income.

RISR vs 10-year US Treasury Yield

Outlook

Every January produces a glut of forecasts about what to expect from financial markets and the economy in the upcoming year. Some of them might even be worth considering, but mostly people make predictions because they are asked, not because they know. We won’t be making a specific forecast, but we would make the following observations.

When we launched RISR in 2021, it seemed a strong probability that rates would have to increase due to clear and undeniable inflationary pressures. That prediction turned out to be a good one, but the current market outlook is far less predictable. While measured inflation has come down materially from the highs of 2022, it is still well above the Fed’s stated 2% target.

We now have two significant military conflicts, and in many ways the war in Gaza could be more destabilizing to economic order than the war in Ukraine, especially if it expands to a second one in Lebanon. For instance, due to attacks on commercial vessels carrying oil and other global commodities and goods, shipping through the Red Sea and the Suez canal has been almost completely halted, and attacks on commercial vessels have occurred in the Persian Gulf as well. If it continues, this puts significant stress on supply chains and imparts inflationary pressures globally.

Despite some minor softness in reported statistics, labor markets remain tight, and wage pressures have barely weakened. Meanwhile, financial conditions have actually loosened in recent months, since approaching neutral earlier in 2023.

Broad measures of economic activity likewise remain relatively strong, and there doesn’t seem to be a recession on the very near horizon, though presumably one will happen eventually. There are a number of other “technical” factors including an enormous amount of upcoming Treasury refundings for this year, and the Fed’s stated goal to reduce the size of its balance sheet, which still has a very long way to go. Both of these will tend to keep upward pressure on long term rates, even if the Fed Funds rate holds at it current level or even is allowed to come down slowly as the Fed itself has stated. Of course, there is the additional uncertainty related to the upcoming presidential election, which seems likely to break all prior records for political volatility.

Consequently, we see a continuation of market volatility, and the potential for rates to surprise to the upside. For that reason, we think it still makes a great deal of sense for a broad range of investors to hold at least a portion of their assets in strategies like RISR, that can dampen overall portfolio volatility without sacrificing current income. While it may be satisfying for some to make bold predictions about a Fed pivot to lower rates, the weight of history doesn’t support that position. Indeed, the greatest likelihood, measured by historical norms is for a normalized yield curve, where long term rates are above short term rates.

Even if the Fed does begin to lower the Fed Funds rate (which is a very short-term rate), that does not imply that longer term rate will follow the same path. The current inversion in the yield curve has persisted longer than any period in the past 40 years. Prudent risk management simply has to consider the likelihood of a normalization that could see long term rates increase even after the Fed makes a pivot.

The obsession in the financial press, and especially on TV outlets such as Bloomberg and CNBC, about when the Fed will start to cut rates, really misses the point. As we noted last month, savvy investors think about a time horizon measured in quarters and years rather than weeks or months, and they need to be prepared for a bumpy ride. Risk management continues to be the correct posture. Managing credit exposure and duration ought to remain top priorities, and we believe RISR can help in that effort. We are happy to speak with any investors seeking more detailed information regarding our holdings and risk/reward profile.

Please contact us to explore how RISR might fit into your overall strategy, to help you manage risk while generating an attractive current yield. And best wishes for a prosperous, healthy and peaceful 2024.

Portfolio Applications

We believe RISR provides an attractive, thematic strategy that provides strong correlation benefits for both fixed income and equity portfolios. It can be utilized as part of a core holding for diversified portfolios or as an overlay to manage the interest rate risk of fixed income portfolios. Alternatively, RISR can be used as a macro hedge against rising interest rates with less exposure to equity beta and negative correlation to fixed income beta. The underlying bonds are all U.S. agency credit that are guaranteed by FNMA, FHLMC or GNMA. There is no financing leverage or explicit short positions that relies on borrowed securities. Also, timing is on our side as the strategy generates current income if interest rates were to remain within a trading range.

Please contact us to explore how RISR can be utilized as a unique tool to adjust your portfolio allocations in the current inflationary environment.

| Yung Lim | Dean Smith | George Lucaci |

|---|---|---|

| Chief Executive Officer | Chief Strategist and Marketing Officer | Global Head of Distribution |

| Chief Investment Officer | RISR Portfolio Manager | |

| ylim@foliobeyond.com | dsmith@foliobeyond.com | glucaci@foliobeyond.com |

| 917-892-9075 | 914-523-2180 | 908-723-3372 |

This material must be preceded or accompanied by a prospectus. For a copy of the prospectus please click here.

Investments involve risk. Principal loss is possible. Unlike mutual funds, ETFs may trade at a premium or discount to their net asset value. The fund is new and has limited operating history to judge fund risks. The value of MBS IOs is more volatile than other types of mortgage related securities. They are very sensitive not only to declining interest rates, but also to the rate of prepayments. MBS IOs involve the risk that borrowers may default on their mortgage obligations or the guarantees underlying the mortgage-backed securities will default or otherwise fail and that, during periods of falling interest rates, mortgage-backed securities will be called or prepaid, which may result in the Fund having to reinvest proceeds in other investments at a lower interest rate.

The Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying assets or index; the loss of principal, including the potential loss of amounts greater than the initial amount invested in the derivative instrument. The value of the Fund’s investments in fixed income securities (not including MBS IOs) will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities owned indirectly by the Fund. Please see the prospectus for a complete description of principal risks.

Diversification does not eliminate the risk of experiencing investment losses.

Index Definitions

Bloomberg Barclays US Aggregate Bond Index: A broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

US Treasury 7-10 Yr Bond Inversed Index: ICE U.S. Treasury 7-10 Year Bond 1X Inverse Index is designed to provide the inverse of the daily return of the ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7). ICE U.S. Treasury 7-10 Year Bond Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market. Qualifying securities of the underlying index must have greater than or equal to seven years and less than 10 years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million.

S&P 500 Index: The S&P 500 Index, or Standard & Poor's 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

IBOXHY Index: iBoxx USD Liquid High Yield Total Return Index measures the USD denominated, sub-investment grade, corporate bond market. The index includes bonds with minimum 1 years to maturity,

minimum amount outstanding of USD 400 mil. Bond type includes fixed-coupon, step-up, bonds with

sinking funds, medium term notes, callable and putable bonds.

Definitions

Alpha: a return achieved above and beyond the return of a benchmark or proxy with a similar risk level.

Annualized Equivalent Yield: represents the annualized yield based on the most recent month of income distribution: (income distribution x 12 months)/price per share.

Basis Points (bps): Is a unit of measure used in quoting yields, changes in yields or differences between yields. One basis point is equal to 0.01%, or one one-hundredth of a percent of yield and 100 basis points equals 1%.

Beta measures: the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index; more than one means greater volatility.

Convexity: A measure of how the duration of a bond changes in correlation to an interest rate change. The greater the convexity of a bond the greater the exposure of interest rate risk to the portfolio.

Correlation: a statistic that measures the degree to which two securities move in relation to each other.

Coupon: is the annual interest rate paid on a bond, expressed as a percentage of the bond’s face value.

CUSIP: An identifier number that stands for the Committee on Uniform Securities Identification Procedures assigned to stocks and registered bonds in the United States and Canada.

Duration: measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

GNMA: Government National Mortgage Association

FNMA: Federal National Mortgage Association

FHLMC: Federal Home Loan Mortgage Corporation

Short Investment (Shorting): is a position that has been sold with the expectation that it will decrease in value, the intention being to repurchase it later at a lower price.

Distributed by Foreside Fund Services, LLC.