RISR Commentary for January 2023

Performance Summary

The FolioBeyond Rising Rates ETF (ticker: RISR) returned -3.89% based on the closing market price (-2.62% based on net asset value or “NAV”) in January. In comparison, the ICET7IN Index (US Treasury 7-Year Bond Inversed Index) returned -3.15% while the Bloomberg Barclays U.S. Aggregate Bond Index ("AGG") returned 3.08% during the same period. Thus, the start to 2023 saw more of the see-saw performance in interest rates we saw throughout 2022.

This most recent market rally was triggered by a series of more benign readings for several closely followed indicators including moderating labor costs, and the growing conviction that the Fed would lower its next rate hike to 25 basis points (bps), down from the recent string of 50 bps hikes last year. Once again, as we saw several times in 2022, the “peak inflation” and “Fed will pivot” crowd gained traction. This belief—mistaken in our view—led to a meaningful rally in equities, especially for the battered technology sector which saw the best returns in nearly 6 months. In a similar risk-on fashion, 10-year Treasury bonds rallied by 37 bps, declining back down to 3.51 from 3.88 at the end of 2022. This was the second largest monthly decline in long-term rates since the beginning of 2021.

This was capped by another disastrous press conference by Federal Reserve Chair Powell that took place on February 1, in which he repeatedly used the word “disinflation” to describe the current market environment. It was rather reminiscent of his prior obsession with the word “transitory” to describe rapidly accelerating inflation in 2021, that the Fed chose to ignore until it was no longer possible to do so. In any case, “disinflation” was exactly the word those expecting a Fed pivot to lower rates wanted to hear. The stock market immediately rocketed higher and rates fell further.

In light of the market moves in January, RISR’s NAV decline of 2.62%, was better than expected. As noted in prior communications, we aim for a negative 10-year duration target. In practice over time, we have achieved something close to that in rising rate periods, but our downside in market rallies has reflected something closer to negative 5-7 years. The empirical duration in January was ‑7.05 years[1]. This is due in part to certain technical factors in the market, where mortgage rates did not move in lockstep with treasuries, and also because the of the asymmetrical response of prepayment speeds and mortgage OAS[2] in rising vs. declining rate environments.

We returned to our stabilized dividend of $0.18/share in January, following a larger year end payment in December. It is our intention to maintain this rate, although it cannot be guaranteed. As of now, the yield on our current portfolio is comfortably above the level needed to maintain that rate.

Outlook

The Fed, through its halting, initially bumbling, response to inflation in 2021, has created quite a challenging set of problems for the economy. Inflation has come down somewhat from the highs of last summer but is still far above the Fed’s target. Moreover, inflationary pressures have migrated from goods (especially oil and used cars) to services and may be becoming embedded in behavior and expectations for service providers and employees.

The labor market remains extraordinarily tight. The chart below shows the number of unfilled job vacancies is still near all-time highs, at more than 11million unfilled positions as of December 2022.

These labor shortages are spread across the economy, both by industry and geography. Some economists believe this is still a hangover effect from the Covid pandemic, while others think something more structural and permanent is happening in the US labor force. Other Western countries are facing similar worker shortages.

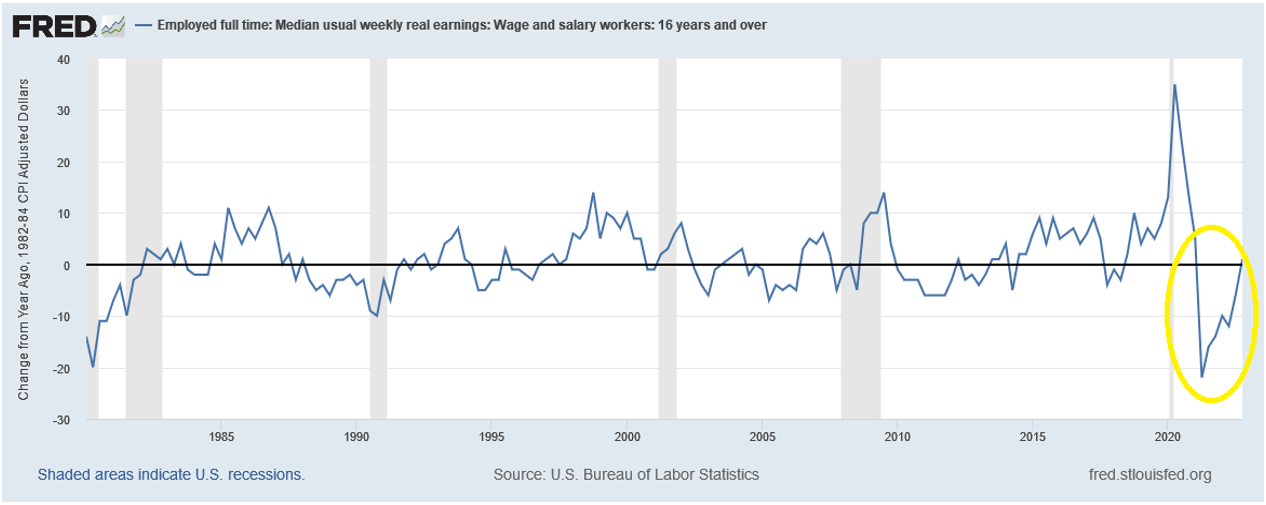

The one proven way to entice potential workers to re-engage with the labor force is through higher wages. This means that in order to bring labor market imbalances back into balance, wages will have to continue to rise. There is a lot of catching up to do. The graph below shows the year over year change in real, inflation-adjusted wages. They have actually been declining significantly since Q1 of 2021. In other words, we haven’t even seen broad-based wage inflation yet. We believe it is coming.

For these reasons, we continue to believe the current Fed tightening cycle has quite a bit further to run. While it is true that this cycle has been more aggressive in terms of the pace of hikes as compared to some earlier episodes, it is also true that we started from a near zero rate, following a multi-decade easing cycle.

Higher for longer, is the somewhat contrarian stance we have taken, and we still think it is the right position for prudent investors and investment advisors. We think it still makes sense to shorten duration, and to be very cautious in adding credit risk. RISR can help in that task.

Even if the Fed decides to slow the pace of their rate hikes from the rapid rises in 2022, that should not be taken as an “all clear” to pile back into risk assets.

We designed RISR to have broad appeal to a range of investors, including those who have a more sanguine view, than ours, but who also agree with the wisdom of prudently managing risk. RISR can help in that effort, offering a low correlation to many key market sectors, together with a high current dividend.

Please contact us to explore how RISR might fit into your overall strategy, to help you manage risk while generating an attractive current yield.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 866-497-4963. Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Returns beyond 1 year are annualized.

A fund's NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the fund was traded. The fund intends to pay out income, if any, monthly. There is no guarantee these distributions will be made.

Total Expense Ratio is 0.99%.

For standardized performance click here

Portfolio Applications

We believe RISR provides an attractive, thematic strategy that provides strong correlation benefits for both fixed income and equity portfolios. It can be utilized as part of a core holding for diversified portfolios or as an overlay to manage the interest rate risk of fixed income portfolios. Alternatively, RISR can be used as a macro hedge against rising interest rates with less exposure to equity beta and negative correlation to fixed income beta. The underlying bonds are all U.S. agency credit that are guaranteed by FNMA, FHLMC or GNMA. There is no financing leverage or explicit short positions that relies on borrowed securities. Also, timing is on our side as the strategy generates current income if interest rates were to remain within a trading range.

Please contact us to explore how RISR can be utilized as a unique tool to adjust your portfolio allocations in the current inflationary environment.

| Yung Lim | Dean Smith | George Lucaci |

|---|---|---|

| Chief Executive Officer | Chief Strategist and Marketing Officer | Global Head of Distribution |

| Chief Investment Officer | RISR Portfolio Manager | |

| ylim@foliobeyond.com | dsmith@foliobeyond.com | glucaci@foliobeyond.com |

| 917-892-9075 | 914-523-2180 | 908-723-3372 |

This material must be preceded or accompanied by a prospectus. For a copy of the prospectus please click here.

Investments involve risk. Principal loss is possible. Unlike mutual funds, ETFs may trade at a premium or discount to their net asset value. The fund is new and has limited operating history to judge fund risks. The value of MBS IOs is more volatile than other types of mortgage related securities. They are very sensitive not only to declining interest rates, but also to the rate of prepayments. MBS IOs involve the risk that borrowers may default on their mortgage obligations or the guarantees underlying the mortgage-backed securities will default or otherwise fail and that, during periods of falling interest rates, mortgage-backed securities will be called or prepaid, which may result in the Fund having to reinvest proceeds in other investments at a lower interest rate.

The Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying assets or index; the loss of principal, including the potential loss of amounts greater than the initial amount invested in the derivative instrument. The value of the Fund’s investments in fixed income securities (not including MBS IOs) will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities owned indirectly by the Fund. Please see the prospectus for a complete description of principal risks.

Diversification does not eliminate the risk of experiencing investment losses.

Footnotes

[1] -7.05 = -2.62% change in NAV ÷ 37 bps change in rates.

[2] OAS, or Option Adjusted Spread, is a measure of mortgage rate spreads over risk free rates that takes into account the response of prepayment incentives as market interest rate change, among other factors.

Index Definitions

Bloomberg Barclays US Aggregate Bond Index: A broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

US Treasury 7-10 Yr Bond Inversed Index: ICE U.S. Treasury 7-10 Year Bond 1X Inverse Index is designed to provide the inverse of the daily return of the ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7). ICE U.S. Treasury 7-10 Year Bond Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market. Qualifying securities of the underlying index must have greater than or equal to seven years and less than 10 years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million.

S&P 500 Index: The S&P 500 Index, or Standard & Poor's 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

IBOXHY Index: iBoxx USD Liquid High Yield Total Return Index measures the USD denominated, sub-investment grade, corporate bond market. The index includes bonds with minimum 1 years to maturity,

minimum amount outstanding of USD 400 mil. Bond type includes fixed-coupon, step-up, bonds with

sinking funds, medium term notes, callable and putable bonds.

Definitions

Alpha: a return achieved above and beyond the return of a benchmark or proxy with a similar risk level.

Annualized Equivalent Yield: represents the annualized yield based on the most recent month of income distribution : (income distribution x 12 months)/price per share.

Basis Points (bps): Is a unit of measure used in quoting yields, changes in yields or differences between yields. One basis point is equal to 0.01%, or one one-hundredth of a percent of yield and 100 basis points equals 1%.

Beta measures: the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index; more than one means greater volatility.

Yield: the return to an investor from the bond's interest, or coupon, payments.

Coupon: is the annual interest rate paid on a bond, expressed as a percentage of the bond’s face value.

Correlation: a statistic that measures the degree to which two securities move in relation to each other.

Convexity: A measure of how the duration of a bond changes in correlation to an interest rate change. The greater the convexity of a bond the greater the exposure of interest rate risk to the portfolio.

CUSIP: An identifier number that stands for the Committee on Uniform Securities Identification Procedures assigned to stocks and registered bonds in the United States and Canada.

Duration: measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

GNMA: Government National Mortgage Association

FNMA: Federal National Mortgage Association

FHLMC: Federal Home Loan Mortgage Corporation

Short Investment (Shorting): is a position that has been sold with the expectation that it will decrease in value, the intention being to repurchase it later at a lower price.

Distributed by Foreside Fund Services, LLC.